Mind The Gap #01

European Tech weekly signal over noise. News, deals, funds, & exits.

📅 January 05 – 09, 2026 | Read time: 5 mins

👋 The Week in Review

Welcome back. If the first week of 2026 is any indicator, the “infrastructure phase” of the AI boom is far from over: it’s just getting more expensive. With Nscale, xAI, and Anthropic all circling multi-billion dollar capital injections, the gap between the AI haves and have-nots is widening into a chasm.

But the real signal for Europe this week lies in FinTech. We are seeing a shift from pure growth to strategic consolidation. Zilch’s acquisition of Fjord Bank isn’t just an expansion; it’s a maturity play, securing banking licenses to own the full value chain. When capital costs are high, the winners buy their way into new markets rather than building from scratch.

Let’s dive into the data.

📰 News of the Week

The Big Story: AI capital expenditure is limitless

Nscale is reportedly in talks to raise $2B (€1.7B), following its $1.1B raise just last September.

Why it matters: This rapid follow-on financing confirms that for AI infrastructure plays, capital is the primary moat. The pace of investment is accelerating, not stabilizing.

US Mega-Rounds: The arms race continues stateside. Claude (Anthropic) is targeting a $10B raise at a $350B valuation with GIC, while xAI secured $20B at a $230B valuation in a deal led by Nvidia.

Meta’s Power Play: Meta has reportedly committed $2B+ to Singaporean AI agent developer Manus, a deal that has sent shockwaves all the way through China.

FinTech: The Consolidation Wave

Zilch acquires Fjord Bank: The UK unicorn is betting €120M on Lithuanian AB Fjord Bank to fuel its European rollout.This follows a stellar year for Zilch: $175M raised, $200M+ revenue, and a second UK payment license.

Payhawk preps for scale: The Bulgarian unicorn is preparing a $100M round at a $2B valuation. With key competitor Brex recently securing its EU license and $1B+ funding, Payhawk is arming itself for a battle over European enterprise spend management.

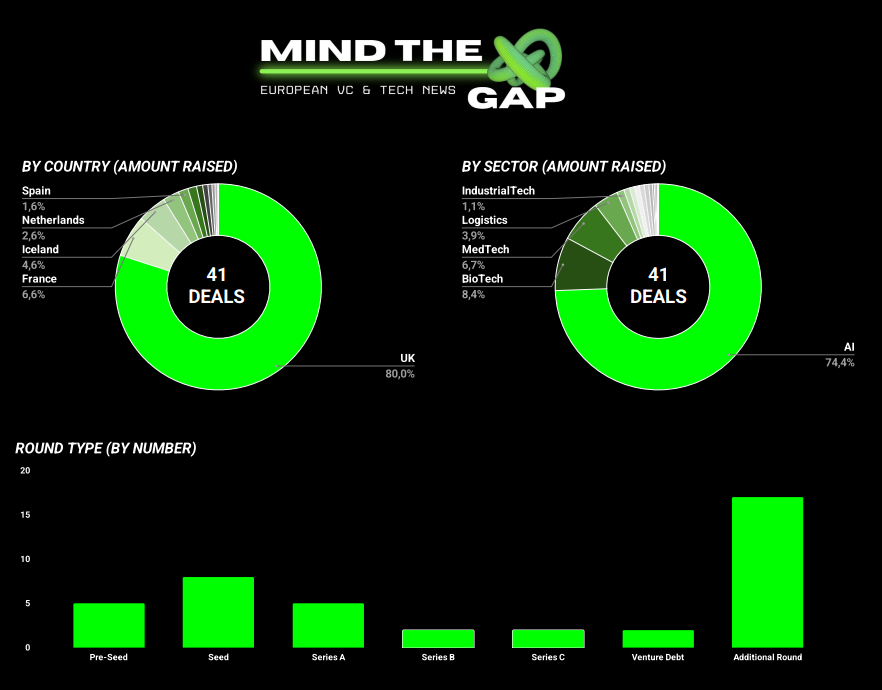

🇪🇺 Deals of the Week

Health and BioTech dominated the narrative this week, capturing nearly 60% of total funding when excluding Global Technical Realty’s €1.6B outlier deal.

🔍 The Deep Dive

BrightHeart (MedTech) | Series A | €11M

The Deal: The Paris-based AI-driven pre-natal ultrasound solutions raised €11M to deliver best-in-class fetal heart screening.

The Investors: Led by Odyssé Venture and GO Capital, with participation from Mussallam, CHD Alliance, Lift Value, IDAO HealthTech Club, Sofinova Partners, and Business Angels.

The Analysis: Ultrasound quality has historically suffered from “operator variability”: the results depended heavily on who was holding the probe. BrightHeart’s AI detects congenital heart defects (CHD) with 96% accuracy, a massive leap for a condition affecting 1.35M newborns annually. Notably, they are the only player in the field with published peer-reviewed clinical evidence and 5 FDA clearances.

What’s Next: Funding will drive US commercialization, European expansion, the scaling of their B-Right AI platform, and the development of their technology to other organs.

Biographica (AgTech) | Growth | €8M

The Deal: London-based platform applying AI drug discovery techniques to crop genetics raised €8M.

The Investors: Led by Faber VC, backed by EQT Foundation, SuperSeed, and others.

The Analysis: Biographica is effectively “applying pharma logic to farming.” By using AI to validate gene control in crops, they can accelerate breeding programs by 12x compared to traditional methods. With climate change pressuring global yields and food security becoming a geopolitical issue, cutting R&D timelines by five years, and thus reducing costs by millions, is a critical commercial and humanitarian unlock.

What’s Next: Expanding the AI platform to new crop traits and deepening commercial ties across the seed industry.

⚡ Deal Flow

🇬🇧 Global Technical Realty (Data Centers) — €1.6B: London-based build-to-suit data center platform secured massive debt/equity facility.

🇬🇧 Swap (Logistics) — €85M Series C: London-based e-commerce operating platform for unified logistics.

🇳🇱 ShanX MedTech (MedTech) — €24M: In-Vitro diagnostic platform for antimicrobial susceptibility testing.

🇧🇪 I-Care (IndustrialTech) — €20M: Predictive maintenance specialist becomes Belgium’s newest unicorn.

🇫🇷 Equitable Earth (ClimateTech) — €12.6M Series A: Certification provider for nature-based carbon projects.

🇦🇹 VitreaLab (DeepTech) — €9.4M Series A: Vienna-based developer of photonic integrated circuits for laser-based AR displays.

🇩🇪 United Manufacturing Hub (IndustrialTech) — €5M Seed: Cologne-based open-source industrial data platform.

👉 See the full database of 40+ rounds from this week: here.

💸 New Dry Powder

Spotlight: Antler (Singapore) — €440M Early-stage specialist Antler announced huge new funds across the US, Europe, and Asia, backed by investors like EIFO. Unlike traditional VCs, Antler prioritizes day-zero intervention and global scale. While 50% of this vintage targets the US, a significant portion is earmarked for Europe following their success with unicorns like Airalo and Lovable.

Thesis: AI, Housing, and BioTech.

Other Fund Launches:

🇵🇱 Future Tech Poland (€350M) — Launched by EIF and BGK to boost the Polish deep tech and innovation ecosystem.

🇪🇸 4Founders Capital (€60M) — Barcelona-based firm launching a specialized Hospitality Tech fund.

Thank you for reading !

This week, the market proved that strategic depth is the defining trend of European and global VC in 2026.

Don’t just read the market: understand it.

If you enjoyed this edition, please consider sharing it with a colleague or friend who should be tracking European VC.

Did a friend forward this to you? Subscribe and get Mind The Gap in your inbox every Friday.

Best,

Agathe